One-Minute Brief

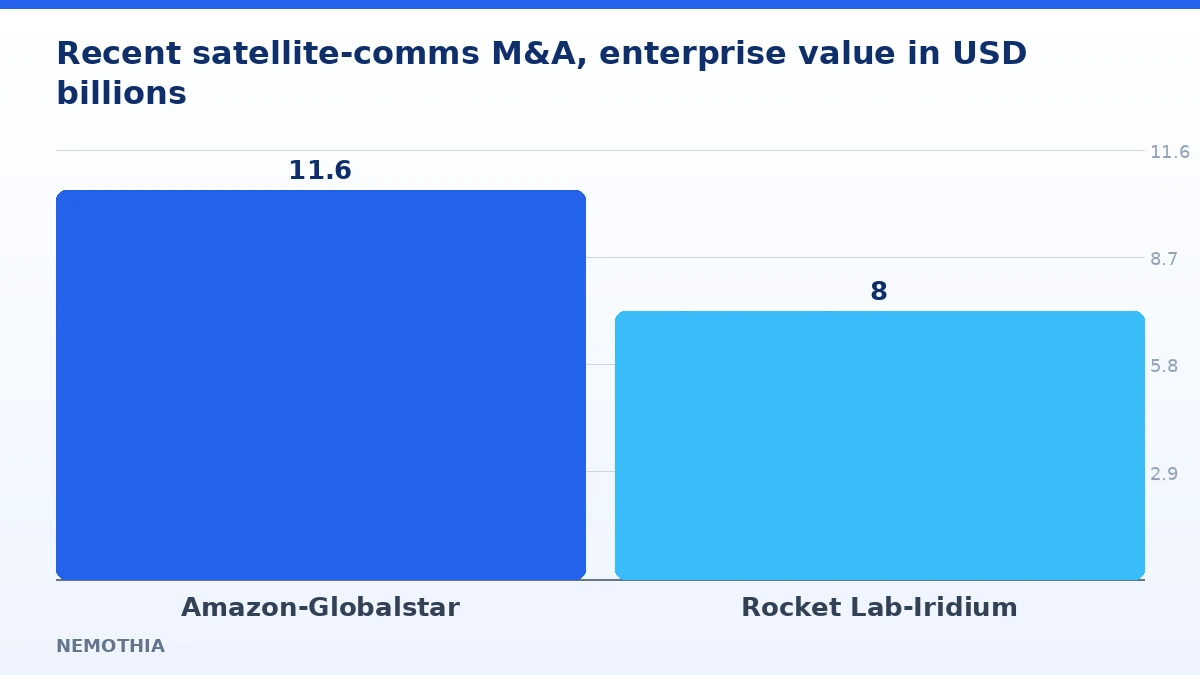

- Rocket Lab agreed to acquire Iridium Communications in a cash-and-stock deal with an enterprise value of approximately $8.0 billion, announced June 29, 2026.

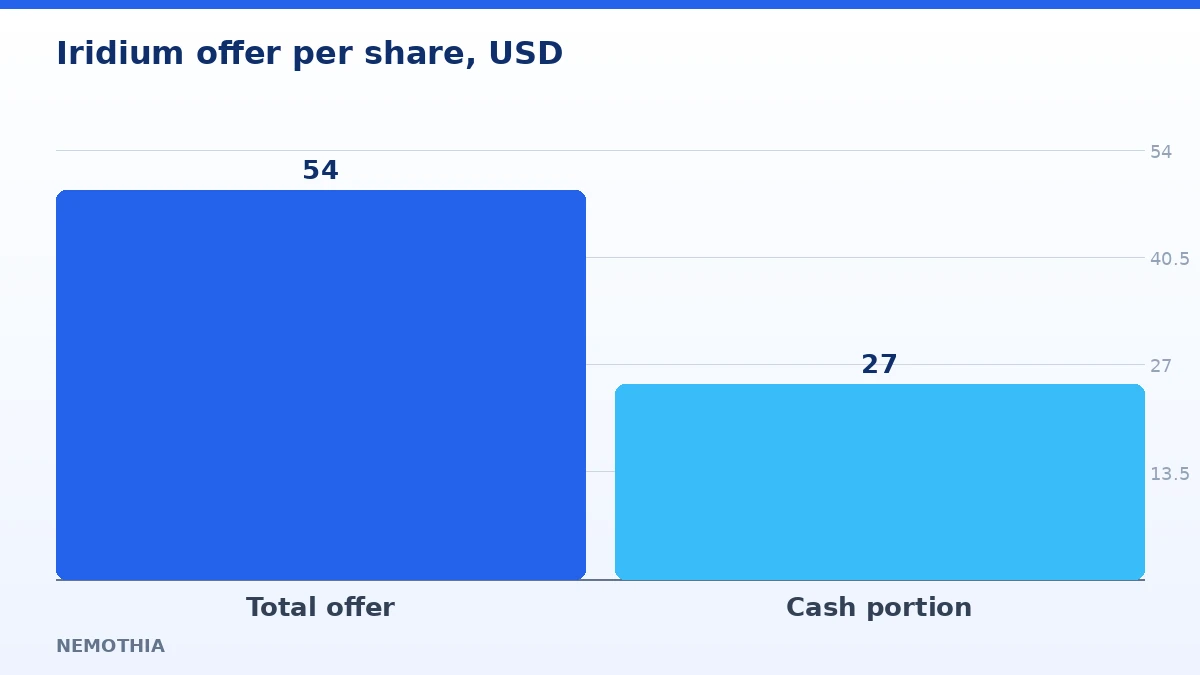

- Iridium shareholders are offered $54 per share, structured as roughly $27 in cash plus Rocket Lab stock.

- To finance the transaction, Rocket Lab secured a bridge loan of around $3.6 billion, according to industry reports.

What Happened

Rocket Lab announced on June 29, 2026 that it would acquire Iridium Communications in a transaction valued at an enterprise value of approximately $8.0 billion. Under the terms, Iridium shareholders would receive $54 per share, composed of about $27 in cash plus shares of Rocket Lab, according to deal summaries. The company disclosed that it arranged a bridge loan estimated at roughly $3.6 billion to fund the cash portion. Iridium shares jumped about 25% following the announcement, consistent with the premium built into the offer.

Strategically, the company framed the deal as creating a fully vertically integrated space business. Rocket Lab brings launch vehicles and satellite manufacturing; Iridium contributes an operating constellation of low-Earth-orbit satellites, licensed spectrum, and a commercial network with more than 500 partners across sectors such as maritime, aviation, and industrial connectivity. Rocket Lab stated the acquisition gives it an immediate foothold in space-based applications including satellite Internet of Things (IoT) and direct-to-device (D2D) services.

The transaction is expected to close in mid-2027, subject to approval by Iridium shareholders and satisfaction of standard regulatory conditions. The move arrives shortly after Amazon’s roughly $11.6 billion acquisition of Globalstar, which closed about ten weeks earlier, underscoring a wave of consolidation in satellite communications. Several outlets framed the combination as an attempt to build a broader challenger to SpaceX’s Starlink, though the two companies operate different network architectures and business models.

Why This Matters for Rocket Lab Iridium

The industry impact is a shift in what “winning” in space looks like. For a decade, the competitive story centered on launch cost – who could put a kilogram into orbit most cheaply. The Rocket Lab Iridium deal reframes the contest around vertical integration: controlling launch, satellite production, spectrum, and the recurring service revenue that comes from operating a network. Owning an in-orbit constellation converts a launch-and-build company with lumpy, project-based revenue into one with a recurring subscription base.

The technical meaning lies in what Iridium actually operates. Its low-Earth-orbit constellation provides genuinely global coverage, including polar regions, and the company holds licensed spectrum that is difficult and slow for newcomers to replicate. That spectrum, combined with an existing D2D and IoT footprint, is arguably the most valuable asset in the deal, because regulatory-grade spectrum rights are a scarce, defensible moat in a field where hardware can be copied but airwave licenses cannot.

Corporate strategy is visible in the financing and the timing. Rocket Lab is taking on a bridge loan of about $3.6 billion to fund the cash component – a figure cited in multiple reports – a significant leverage step for a company of its size. The willingness to stretch financially indicates management views owning an operating network as strategically necessary rather than optional.

Coming so soon after Amazon’s Globalstar purchase, the deal also suggests that established players believe the window to acquire scarce orbital assets is closing as valuations rise – a capital-allocation shift that echoes the race to lock up scarce compute and foundry capacity elsewhere in tech.

The market change is consolidation. Two multibillion-dollar satellite-communications acquisitions within roughly ten weeks – Amazon-Globalstar and Rocket Lab-Iridium – indicate that the sector is moving from fragmented specialists toward integrated platforms. For remaining independent operators, the strategic question becomes whether to partner, sell, or invest heavily to stay competitive against vertically integrated rivals with their own launch capacity.

The cross-industry ripple extends well beyond aerospace. For telecom carriers, an integrated Rocket Lab-Iridium with direct-to-device capability intensifies the emerging competition to connect ordinary phones from space, pressuring carriers to strike or deepen their own satellite partnerships. For defense and government users, a vertically integrated Western provider with sovereign launch, manufacturing, and spectrum becomes a more attractive supplier of resilient communications, which could redirect procurement toward integrated vendors.

And for logistics, maritime, and aviation operators that already depend on Iridium for tracking and connectivity, ownership by a launch company raises both an opportunity – faster constellation refresh and capacity growth – and a dependency risk if service priorities shift toward new markets.

Global market reaction was most visible in Iridium’s roughly 25% share-price jump, but the broader signal read across US and international markets was structural: investors and analysts treated the deal less as a one-off and more as confirmation that the space economy is entering a consolidation phase in which operating networks, not just rockets, are the prize.

Risks & Counterpoints

- The deal is not closed; it requires Iridium shareholder approval and regulatory clearance and is not expected to complete until mid-2027, leaving time for terms or conditions to change.

- A bridge loan of roughly $3.6 billion adds meaningful leverage, and integration of an operating network into a launch-and-manufacturing firm carries execution risk.

- The “Starlink challenger” framing may overstate near-term reality; Iridium’s narrowband, global-coverage network serves different use cases than Starlink’s broadband constellation.

- Regulators reviewing spectrum transfers and defense-relevant assets could impose conditions, particularly given the strategic value of licensed orbital spectrum.

- Cash-and-stock consideration means Iridium holders’ ultimate value depends partly on Rocket Lab’s post-deal share performance, not a fixed cash figure.

What’s Next for Rocket Lab Iridium

- Whether Iridium shareholders approve the deal and how regulators treat the spectrum and defense-relevant assets – this determines if and how the transaction closes.

- How Rocket Lab manages the roughly $3.6 billion of bridge financing and any refinancing – leverage will shape its flexibility through the mid-2027 close.

- Whether additional satellite-communications deals follow – a third large transaction would confirm the consolidation trend rather than two isolated moves.

Bottom Line

My Take: The Rocket Lab Iridium deal is best understood as a bet that the durable value in space is shifting from launching hardware to owning the networks and spectrum that generate recurring revenue. At roughly $8 billion and financed partly with a sizable bridge loan, it is an aggressive move that converts Rocket Lab from a launch-and-build specialist into an integrated operator – if it clears shareholders and regulators by its expected mid-2027 close. My Take: the most important number here is not the $8 billion price but the ten-week gap between the Amazon-Globalstar and Rocket Lab-Iridium deals. The zoom-out that outlasts this news cycle is that scarce orbital spectrum and operating constellations are being locked up quickly – which means telecom carriers, defense buyers, and the logistics, maritime, and aviation industries that depend on satellite connectivity should be watching who owns the pipes above them, because those ownership decisions will shape the cost and availability of connectivity on the ground for years.

Frequently Asked Questions

What is the Rocket Lab Iridium deal worth?

Rocket Lab agreed to acquire Iridium Communications for an enterprise value of approximately $8.0 billion in a cash-and-stock transaction. Iridium shareholders are offered $54 per share, structured as roughly $27 in cash plus Rocket Lab stock.

Why does the Rocket Lab Iridium acquisition matter for the space industry?

It moves the competitive focus from cheap launch toward vertical integration – owning launch, manufacturing, spectrum, and an operating network with recurring revenue. It also marks the second multibillion-dollar satellite-communications deal in about ten weeks, signaling sector consolidation.

When will the Rocket Lab Iridium deal close?

The companies expect the transaction to close in mid-2027, subject to Iridium shareholder approval and standard regulatory clearances. Until then the terms remain contingent.

Is this a direct competitor to SpaceX Starlink?

Some coverage frames it that way, but Iridium’s global, narrowband network serves different use cases than Starlink’s broadband service. The overlap is clearest in emerging direct-to-device connectivity rather than home broadband.

Sources

- investors.rocketlabcorp.com — Official deal announcement, terms, vertical-integration rationale, close timing (2026-06-29)

- sec.gov — Iridium SEC 8-K exhibit on the transaction (2026-06-29)

- sec.gov — Rocket Lab SEC 8-K exhibit on the transaction (2026-06-29)

- govconwire.com — $8B cash-and-stock structure and $54 per-share terms (2026-06-30)

- fool.com — Market impact, Globalstar comparison, share reaction (2026-07-04)

- labusinessjournal.com — Financing and the scale of the bet (2026-07-02)

- congress.net — Bridge loan, Starlink-challenger framing, share pop (2026-07-01)

This article is for informational and educational purposes only and does not constitute investment, financial, or legal advice.